Buying a home is a big part of the American dream. A home where you can build memories with your family and friends that will last forever. Your home most likely to be the largest purchase you will ever make. One of the benefits of being a homeowner is that it will enable you to get a large sum of money if an unexpected expense occurs. Two ways you can take money out of your home is through a home equity loan or a home equity line of credit (HELOC).

What is the Difference Between a HEL and a HELOC?

Home Equity Loan Versus Line of Credit: Pros and Cons

A home equity loan is when you borrow money based on the amount of equity in your home. Your home is used as collateral, and your loan has a fixed interest rate. A HELOC is like using your home’s like a credit card. You can use it whenever you need the money. You do not have to make any monthly payments on a HELOC until you use some or all the money. HELOCs have a variable interest rate, and your house is used as collateral.

What is a Credit Score?

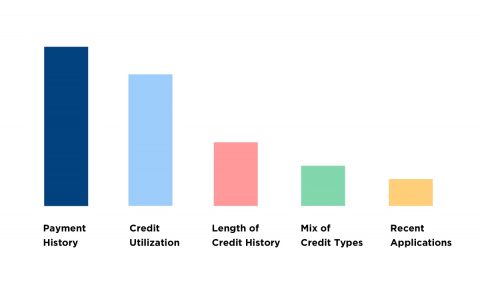

What Factors Affect Your Credit Scores?

When you go to a lender for a home equity loan or a HELOC, they will look at your credit report. One of the first things they will see is your credit score. Your credit score is a numerical representation of how likely you will pay back your debt. The credit score range is between 300-850. If you have a high credit score, you are more likely to receive a favorable interest rate and loan terms. Your score will fall into one of five general categories:

- Poor: 300-579

- Fair: 580-669

- Good: 670-739

- Very Good: 740-799

- Excellent: 800-850

Equifax, Experian, and TransUnion are the three credit bureaus. They each use different criteria in creating a credit score, so the numbers in each category will slightly vary.

Can You Get a Home Equity Loan or HELOC with Bad Credit?

HELOC Calculator: How Much Could You Borrow?

It is possible for you to get a home equity loan or HELOC if your credit score is fair or better, but nearly impossible if you have a poor credit score. Lenders generally like you to have a credit score of at least 620. No matter what your score is, the one thing that will help you get the loan or line of credit is your home. Your home is used as collateral, so if you do not pay back your loan or line of credit, you will lose your home.

Lenders will also look at two other factors. First, you must have equity in your home. You can borrow up 80 percent of your home’s equity value based on the loan-to-value ratio. For instance, any reputable lender or mortgage company will tell you if your home is valued at $400,000 and you owe $250,000, then your lender will use this simple calculation:

- $400,000 x .80 = $320,000 – $250,000 = $70,000 loan amount

Second, your lender will look at your debt-to-income ratio. The amount of debt you carry compared to your income has a huge effect on your credit score and ability to get a loan. You should pay down your debts as much as possible before you apply for a home equity loan or HELOC.